Accommodating mobile payment app users today generally entails the procurement of NFC-compatible PIN pads from POS dealers and integrating those devices with existing POS systems. Adoption for NFC-based mobile payments is definitely growing, but has so far been slower than expected in the US, so it’s likely that mobile payments will continue to evolve to better fit the needs of the mobile user.

Payment integration developers are currently implementing technology that enables smartphone users to connect directly to a merchant’s Point of Sale to pay for goods and services. How soon will these transactions become commonplace? As a POS developer, what are you going to have to do to support those interactions?

Mobile wallets are becoming more popular

Before getting into what you’ll have to do to support smartphone-integrated payments, it’s worth asking whether shoppers and diners are even taking advantage of mobile payment apps.

It turns out that mobile wallets aren’t just a fad. Accenture’s 2016 North American Consumer Digital Payments Survey found that consumer debit card and cash use is declining year over year. The researchers asked 4,000 consumers whether they used digital payments today and if they intended to do so in 2020. Here’s what they found:

Only 16 percent of consumers use mobile payment apps from retailers or restaurants, but 21 percent intend to do so in three years.

Nearly one-fifth (22 percent) intend to use mobile wallets developed by card networks (Visa and MasterCard).

Are these the big numbers that would warrant a massive overhaul of a retailer’s payment infrastructure? Probably not, but as mobile wallet technology matures, usage may be much greater than anticipated three years from now.

Why consumer-based mobile payments may grow

When asked why they didn’t use mobile wallets, 37 percent of Accenture respondents said their cash and plastic cards meet their needs, indicating that mobile wallets, while easy to use, aren’t convenient enough to encourage them to change a common habit. Why whip out a phone when cash will do just fine?

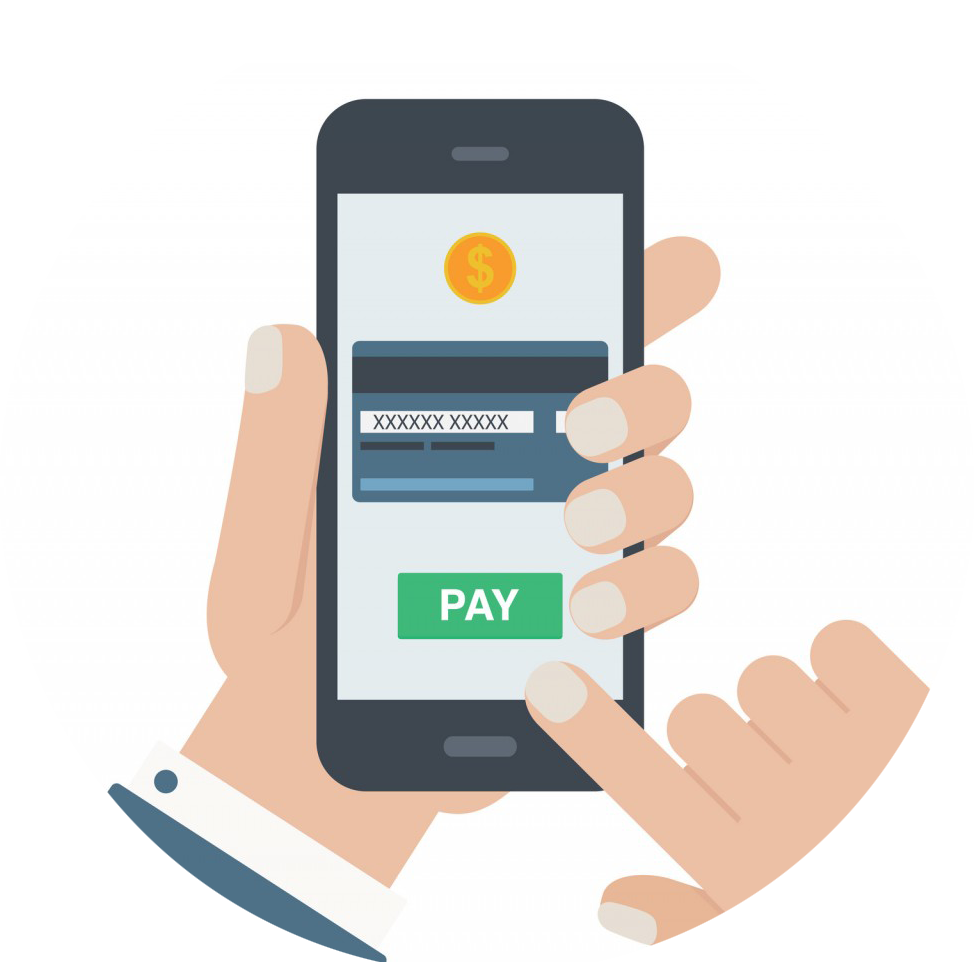

Put yourself in the customer’s seat for a moment. You’re at a restaurant, and the server hands you a mobile PIN pad that either swipes your card or accepts a smartphone payment via NFC. For the sake of argument, let’s say you decide to use Android Pay. If you want to charge the bill to your debit card, you’re going to have to enter the PIN you set up with your bank. In this case, what’s the difference between swiping or dipping your debit card?

Now imagine a server never brings a PIN pad to your table. Instead, he says you can pay the bill online. You open your smartphone, connect to the POS system to view your bill, enter a tip and pay it. You didn’t have to enter a PIN or wait for the server to bring over the PIN pad. And, merchants save dramatically by avoiding the implementation of an army of mobile PIN Pads.

How to integrate merchant POS systems with consumer smartphones

Enabling consumer-based mobile transactions depends on the capabilities and technology at your disposal. Logically, you’d imagine you’d have to build a mobile application connected to the brand you work with. Unfortunately, the concept of branded mobile apps for merchants hasn’t taken off. Users simply don’t want to download a dedicated application for each restaurant or retailer they visit.

Large retailers and restaurant chains might have better luck incentivizing an app download, but what if you’re a small to medium sized business? Fiscally, it may not make sense for a regional restaurant or mom-and-pop store to invest in its own proprietary mobile payment app, especially if you can’t guarantee customer adoption. After all, CSIMarket found net profit margins for restaurants stood around 6.9 percent in the fourth quarter of 2016, so restaurateurs are generally looking to cut costs instead of adding to them.

One of the most cost-effective options is to provide customers with receipts containing URLs or QR codes that direct them to secure e-commerce sites. In this case, diners would either scan QR codes or enter URLs into a mobile browser. Once the code or URL directs them to the site, they can choose to pay with either credit, Apple Pay or any other mobile wallet they have installed on their device. Once the transaction is complete, customers can leave whenever they wish.

Consumer-based mobile payments should be part of a broader omnichannel strategy implemented by merchants who want to remove payments friction for their customers by providing a streamlined in-store, ecommerce and mobile experience.

At the end of the day, you’re going to need some support from a third party. Look for payment integration partners that do much of the heavy lifting and provide technology that requires little-to-no POS system adjustment.