We’re six months past the EMV liability shift deadline – how have things changed? For one, merchants are now on the hook for fraudulent transactions if they haven’t yet integrated and certified their EMV-supported point-of-sale systems. Second, consumers understand what EMV is and the benefits that chip-based payment cards offer. But how many Americans actually use EMV regularly? Better yet, are merchants even accepting these new payment cards, and what’s happened to those that haven’t?

Let’s take a look at the state of EMV adoption with respect to consumers and merchants, now that we’re six-months removed from the liability deadline. The layout of the EMV landscape might surprise both shoppers and businesses.

Who’s got the cards?

One of the biggest EMV adoption hurdles to clear in the past few months has been convincing consumers that these payment cards are beneficial, let alone explaining how the technology actually works compared to mag-strip cards. But things are shaping up.

“51% more consumers have EMV-based cards than did on Oct. 1, 2015.”

Issuers have been trying to get EMV credit and debit cards into shoppers’ wallets since the beginning of 2015, but since October 1 of that year, they’ve made great strides. According to CardHub, approximately 40 percent of Americans received a new payment card with an embedded EMV chip. And Mastercard reported that this increase could be as a high as 51 percent. It seems as though consumers are ready for EMV.

In fact, much of the trepidation to EMV has diminished on the cardholder front. Fifty-nine percent of EMV payment card users participating in a CreditCards.com survey asserted that they don’t have any complaints.

Unfortunately, that doesn’t necessarily mean that consumers are using their EMV chip-based cards at POS. The CardHub report found that around 40 percent of shoppers have never paid with these cards in the manner that was intended (i.e. inserting the chip end of the card).

Merchants are far from ready

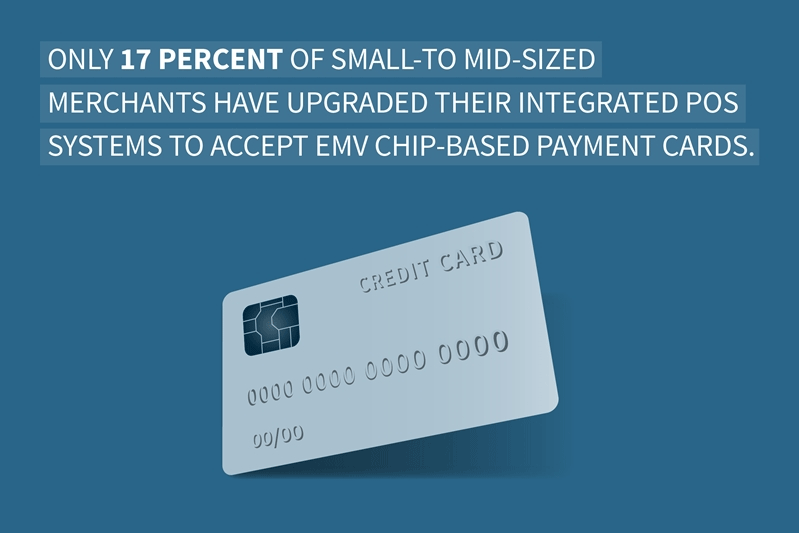

Businesses simply aren’t ready for EMV despite it being more than six months since the liability deadline has passed. According to a survey conducted by PiperJaffray for Datacap, only 17 percent of small- to mid-sized merchants have upgraded their integrated POS systems to accept EMV chip-based payment cards. Industry-specific EMV-adoption rates vary, but none are close to impressive, and retailers and restaurants are among the EMV adoption laggards.

Even major retailers are dragging their feet on integrating certified EMV systems with their POS environments, despite many stating that they were on track for the October 1 deadline. CardHub noted that only around 60 percent of those bigger merchants have actually upgraded their POS terminals to support the new payment method.

The mistake

To put it bluntly, the realities of forgoing EMV adoption are harsher than many merchants anticipated. In many cases, those businesses that have yet to integrate EMV support have seen fraud rates rise.

Kroger’s Chief Financial Officer stated that the grocery store chain has seen its operating costs climb right after the liability shift took place, according to Paymentssource, and the most expensive chargebacks are to blame. This report jives with quotes collected by First Annapolis from many acquirers.

“Our … December chargebacks increased 3.8 times normal, all from non-EMV merchants,” said a top twenty non-bank acquirer. “And it was in areas you would not normally see chargebacks – $8 ticket at a deli; $25 ticket at a grocery store.”

“Fraudsters are making the most out of thier limited timelines.”

Now, Kroger’s is about 93 percent EMV compliant, CardHub’s data indicated, so it’s not liable for all fraudulent transactions. That said, other merchants are still on the hook if they haven’t integrated and certified all of their EMV systems within their POS environments. Mark Horwedel, CEO of the Merchant Advisory Group, told Paymentssource that fraudsters realize their opportunity to commit in-person fraud will soon cease to exist, and as such, they plan to go out with a bang – so to speak.

When they could be earning revenue

Besides the clear downside to postponing EMV compliance, there are some benefits that merchants could experience if they act fast and integrate. For example, those with EMV cards are typically the same consumers who want to spend. CreditCards.com found that 76 percent of college graduates, 74 percent of Americans who earn over $75,000 every year and 74 percent of those aged between 18 and 29 years who participated in the survey have EMV chip-based payment cards. Those demographics are among the most willing to spend, and if they cannot complete transactions in a secure manner, they might take their business elsewhere.

All said and done, the state of EMV adoption is positive on the consumer side, but merchants are certainly lacking and failing to adapt to the times. There’s a price to pay for not having a certified POS system that supports EMV, and there’s something to gain in that regard as well. Simply put, the ball is in merchants’ court.